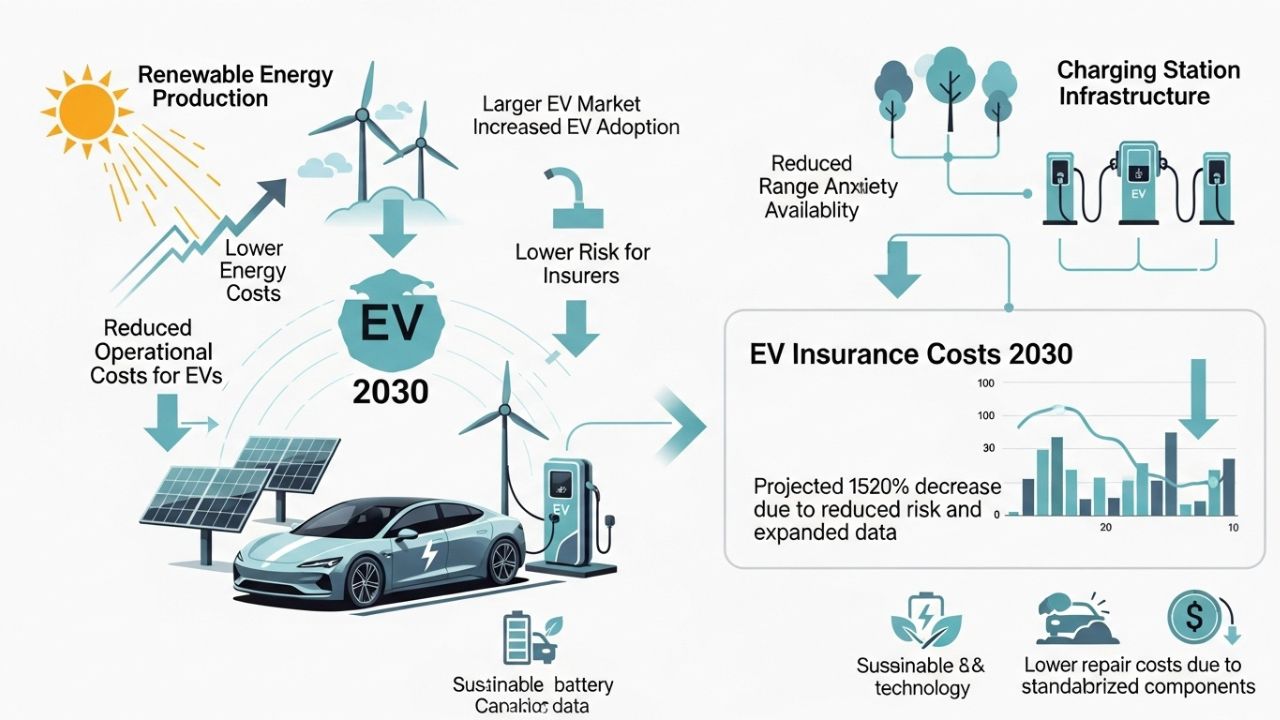

How Renewable Energy and Charging Stations Influence EV Insurance Costs by 2030

The global shift toward electric vehicles (EVs) is more than just a change in the type of cars we drive—it represents a complete transformation of the energy, mobility, and insurance sectors. Unlike traditional fuel-based cars, EVs rely on electricity, increasingly sourced from renewable energy. This energy transition has created an entirely new dimension for insurers: the link between renewable charging infrastructure and EV insurance costs.

As governments pour investments into solar-powered charging hubs, wind-integrated charging stations, and smart electric grids, insurers are starting to factor renewable integration into their risk models. By 2030, the availability, safety, and efficiency of renewable-powered charging stations could significantly impact how much EV owners pay for coverage.

Let’s break down how renewable energy adoption and charging infrastructure affect EV insurance premiums, risks, and future trends.

The Growing Role of Renewable Energy in EV Charging

EV adoption is closely tied to the expansion of renewable-powered charging stations. Instead of relying only on fossil-fuel-derived electricity, governments and utility companies are creating green charging corridors that combine solar panels, wind farms, and energy storage systems.

For insurers, this shift opens new coverage areas:

- Sustainability Incentives: EV owners using renewable-powered charging may be rewarded with lower premiums due to cleaner energy usage.

- Infrastructure Reliability: Stable renewable integration reduces risks linked to charging delays, system overloads, or failures.

- Microgrid Dependence: Off-grid solar and wind charging hubs provide resilience but also create unique liability risks if malfunctions occur.

By 2030, renewable charging won’t just be an eco-friendly option—it will be a critical driver of EV insurance pricing dynamics.

Read Also: A Fresh Look at EV Charging Stations Near You in New York 2025

Charging Infrastructure Risks and Insurance Implications

Insurance is built on assessing risks, and EV charging introduces new ones:

- Charger Damage & Liability: If a solar or wind-powered charging station malfunctions and causes an electrical fault, who is liable—the EV owner, the station operator, or the grid provider?

- Energy Theft Risks: As EV charging is increasingly networked, cyberattacks and illegal power siphoning could impact both operators and drivers.

- Weather-Related Risks: Renewable-powered chargers, often exposed to outdoor environments, are vulnerable to lightning, floods, or storms—affecting insurance underwriting.

- Home Charging Systems: Home-based renewable setups (like rooftop solar with EV chargers) add another layer of property-insurance overlap.

Insurers are already adapting to these scenarios, and by 2030, many policies may include bundled home + vehicle + renewable energy coverage.

Cost Dynamics: Why Charging Stations Affect Premiums

The type of charging station you use—fast charging, solar hubs, or public high-voltage stations—can influence insurance costs:

- High-Voltage Fast Chargers: These stations accelerate battery wear, increasing replacement risk, which may lead to higher insurance premiums.

- Renewable-Powered Stations: Insurers may offer discounts to encourage drivers to use green-powered chargers, aligning with sustainability goals.

- Public vs. Private Charging: Public stations come with risks like vandalism or accidental equipment damage, impacting claim patterns. Private, renewable-energy-driven chargers may be seen as lower risk, reducing insurance costs.

By linking driving habits with charging behaviour, insurers are adopting more refined models for premium calculation.

Vehicle-to-Grid (V2G) Technology: A Two-Way Risk Factor

One of the most exciting developments in charging is vehicle-to-grid (V2G) integration, which allows EVs to not only draw electricity but also supply power back to the grid.

For insurance, this creates both opportunities and challenges:

- Opportunities: EV owners can monetize stored renewable energy, lowering their overall transport costs.

- Challenges: Insurers must cover risks of grid overload, energy transaction errors, and hardware damage linked to V2G use.

Policies by 2030 may specifically address battery stress and grid-related losses, shaping new coverage standards.

How Renewable Incentives Could Lower Future Premiums

Governments promoting clean mobility may collaborate with insurers to reward eco-conscious EV drivers. Possible incentives include:

- Tax-Linked Insurance Discounts: Drivers using renewable-only charging could qualify for reduced premiums.

- Green Bonus Programs: Similar to “no-claim bonuses,” EV policies may include eco-bonuses for charging from certified renewable sources.

- Carbon Credit Tie-Ins: Some insurers might participate in carbon credit markets, sharing financial benefits with policyholders.

This integration means insurance won’t just protect drivers, but also encourage sustainability.

Cybersecurity Risks at Renewable Charging Stations

With renewable charging hubs connected to smart grids, cybersecurity risks emerge as another premium factor. Hackers targeting solar-powered EV charging networks could disable entire corridors or manipulate billing systems.

Insurance evolution will need to cover:

- Malware Attacks on Chargers: Protection against remote shutdowns or hacking attempts.

- Data Privacy Breaches: EV-driver data stored within renewable charging networks.

- IoT Integration Vulnerabilities: Risks tied to interconnected solar, wind, and battery storage systems within charging stations.

Thus, insurers will increasingly invest in cyber-protection partnerships to safeguard ecosystems.

Regional Differences in Renewable Adoption Impact Premiums

Insurance premiums by 2030 will vary depending on regional renewable integration:

- Developed Markets (Europe, North America): Widespread renewable-powered charging may lead to relatively lower average premiums due to stable, sustainable energy networks.

- Developing Nations (Asia, Africa): Slower renewable adoption may keep premiums higher, as risks tied to unreliable charging infrastructure remain significant.

- Global Ports and Trade Hubs: EV fleets in renewable-mapped logistics sectors may enjoy bulk policy discounts linked to green infrastructure usage.

This highlights how location and energy mix will directly impact EV insurance costs.

Read Also: Do EV Batteries Lose Capacity Over Time?

Future Outlook: Insurance as a Driver for Clean Mobility

The relationship between renewable energy, charging stations, and insurance is more than financial—it’s about shaping sustainable transport systems. By 2030:

- EV insurance will reward green charging practices.

- Charging networks will be integrated into policy frameworks.

- Premiums will reflect not just driver behavior—but also energy behavior.

Insurance companies that embrace this green transition stand to move from being passive risk-takers to active enablers of sustainable mobility.

Conclusion

The rise of renewable energy and EV charging infrastructure is transforming the way insurers assess risks and design policies. Charging behavior, renewable integration, cybersecurity, and regional infrastructure will all influence premium calculations by 2030.

For drivers, this means more than just cheaper energy—it could mean lower insurance costs when connected to clean, safe, and reliable charging systems. For insurers, it’s a chance to redefine their role in supporting sustainability, encouraging smarter energy habits, and ensuring mobility remains both safe and affordable.

The future is clear: renewable-powered charging doesn’t just drive EVs—it drives down insurance costs and accelerates the global shift to greener transport.

1 thought on “How Renewable Energy and Charging Stations Influence EV Insurance Costs by 2030”