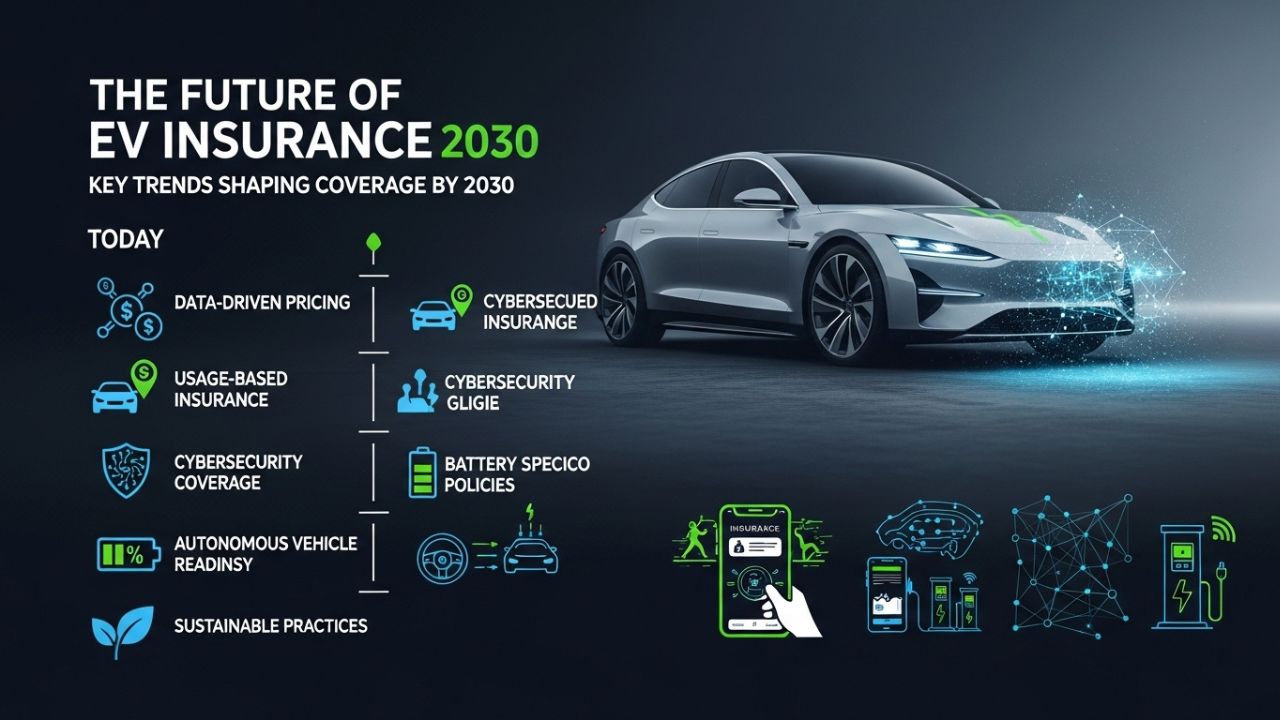

The Future of EV Insurance: Key Trends Shaping Coverage by 2030

The electric vehicle (EV) market is evolving at lightning speed, reshaping not only how people drive but also how the insurance industry prepares for the next decade. With governments pushing for sustainable mobility, automakers committing to fully electric fleets, and charging infrastructure improving across the globe, the number of EVs on the road is expected to skyrocket by 2030.

But with this surge comes pressing questions: How will insurance companies adapt to an electric future? What risks and opportunities will EVs present by 2030? And most importantly, how will premiums, claims, and coverage look different compared to today?

Let’s dive deep into the future of EV insurance and what trends will dominate by 2030.

EV Adoption Will Drive Tailored Insurance Products

By 2030, EVs are projected to account for more than 50% of new car sales in many developed countries. Traditional car insurance models—largely designed around internal combustion engine (ICE) vehicles—will no longer be suitable for EVs with unique risk profiles.

- Specialized Coverage: Insurers will offer policies designed specifically for EV systems, like coverage for high-voltage batteries, charging station equipment, and software protection.

- Custom Premium Models: As EV repairs differ significantly from ICE vehicles, insurers will adjust to reflect labor costs, parts availability, and advanced technology requirements.

Read Also: A Fresh Look at EV Charging Stations Near You in New York 2025

Battery Risks Will Be a Key Focus

The battery pack is the single most valuable component of an EV, often accounting for 30-40% of the car’s total cost. Insuring it presents unique challenges:

- Fire & Damage Risks: Unlike traditional engines, EV batteries can pose thermal runaway risks, requiring high-cost replacement instead of repair.

- Degradation Coverage: Policies may include protection against gradual battery performance loss, offering customers peace of mind as technology evolves.

- Circular Economy Incentives: By 2030, insurers may even reward customers for opting into battery recycling or refurbishment schemes, lowering overall premiums.

Advanced Driver Assistance Systems (ADAS) and Autonomy Will Change Claim Trends

Most EVs today come equipped with advanced driver assistance systems like lane-keeping, collision warnings, and self-parking features. By 2030, partial or full autonomous driving may be widespread in EVs. This will radically alter accident patterns:

- Fewer Accidents, Higher Repair Bills: Improved safety features could drastically lower accident frequency. However, repairs will be expensive due to reliance on sensors, cameras, and AI-driven modules.

- Shift in Liability: If autonomous driving becomes standard, responsibility may shift from drivers to automakers or software providers. Insurers will need to redefine liability models and perhaps even collaborate directly with EV manufacturers.

Cybersecurity Will Become a Critical Aspect of EV Insurance

Unlike traditional vehicles, EVs are essentially “computers on wheels.” By 2030, software-driven EVs will rely heavily on constant connectivity, over-the-air updates, and integration with smart grids.

- Hacking & Data Theft Risks: Insurers may need to cover risks arising from cyberattacks, such as hackers disabling vehicle functions or stealing sensitive user data.

- Digital Identity Protection: Policies might evolve to include personal data coverage, recognizing the privacy risks associated with cloud-connected EVs.

- Collaborations with Tech Firms: Expect insurance companies to partner with cybersecurity firms to build trust and guarantee higher protection levels.

Telematics and Usage-Based Insurance (UBI) Will Become Standard

With EVs equipped with real-time tracking and data-sharing capabilities, insurance companies will increasingly rely on telematics-based risk assessment by 2030.

- Pay-as-You-Drive Models: Policyholders may pay premiums based on actual mileage, driving behavior, and charging habits, rather than flat rates.

- Eco-Friendly Incentives: Safer, smoother driving and responsible charging could lead to discounts, rewarding eco-conscious behaviors.

- Personalized Policies: Unlike generic ICE coverage, EV drivers will enjoy highly individualized insurance experiences.

Impact of Government Regulations and Climate Policies

Global climate targets and EV adoption mandates will also influence insurance structures. By 2030, governments may enforce:

- Mandatory EV Coverage Standards: Ensuring fair and transparent premium models for all users.

- Green Insurance Benefits: Regulators could incentivize insurers to offer discounts for sustainable mobility adoption.

- Cross-Border Harmonization: As EV adoption grows worldwide, cross-country insurance norms may emerge, simplifying global travel with EVs.

Integration of Charging Infrastructure into Coverage

As EV charging networks expand, insurance will also adapt to cover this ecosystem. Key trends include:

- Charging Station Liability: Insurers will offer specialized products covering damage, theft, or power surges at public and private EV charging stations.

- Home Charger Protection: Policies could extend to include installation safety, maintenance, and high-voltage equipment replacement.

- Energy Grid Integration: As vehicle-to-grid (V2G) models mature, insurers will protect both consumers and utility companies from risks tied to energy feedback loops.

Read Also: How Safe Are EV Batteries? Understanding the Risks and Safety Measures of Electric Vehicle Batteries

Cost Dynamics: Will EV Insurance Be Cheaper or More Expensive by 2030?

This is the million-dollar question for consumers—and the answer is nuanced:

- Short-Term Premiums Higher: In the near term, EV insurance costs more due to high repair bills, costly batteries, and limited EV repair expertise.

- Long-Term Premiums Lowering: By 2030, as economies of scale kick in, battery costs fall, and repair networks expand, overall premiums are expected to decline.

- Balance of Safety vs. Cost: Safer vehicles with autonomous functions will balance out the expensive repair bills, creating more competitive insurance pricing.

Conclusion

By 2030, the insurance industry will look dramatically different in response to the rapid rise of electric vehicles. Battery coverage, cyber risks, autonomous driving claims, charging infrastructure, and personalized telematics-based policies will dominate the EV insurance landscape.

For consumers, this means more customised, data-driven, and eco-sensitive coverage options. For insurers, it’s both a challenge and an opportunity to reinvent traditional models, collaborate with automakers, and embrace next-generation technologies.

The shift toward sustainable mobility is inevitable, and insurance companies that anticipate EV-specific challenges today will stand out as leaders in 2030’s electric future.

2 thoughts on “The Future of EV Insurance: Key Trends Shaping Coverage by 2030”